LTC Bullet: The $97 Trillion LTC Paradox Friday, December 5, 2025 Seattle— LTC Comment: Public policy incentivizes accumulating wealth, but discourages spending it on private long-term care (LTC). We explain after the ***news.*** *** REGISTRATION IS NOW OPEN for the 2026 Intercompany Long Term Care Insurance (ILTCI) Conference! Organizers report: “Our in-person conference March 8-11, 2026 at the Rosen Shingle Creek in Orlando, FL is now accepting attendee registrations! As always, our agenda will include numerous educational sessions over two days across seven tracks with ample time for networking and reconnecting with colleagues. Everyone who's anyone in Long Term Care Planning will be there. What about your company? Early Bird Attendee Pricing available now!” Damon and I will be there to work and cover the conference, respectively. Register here. *** *** MORE ILTCI NEWS: 2026 Session Titles & Descriptions announced. “The wait is over! Our amazing Program & Education Committee has put together a stellar lineup of sessions for 2026. These 48 sessions will be scheduled for Monday and Tuesday of the conference. Click this link to see the full list, descriptions, and a one page PDF you can share with your friends and coworkers.” PLUS THIS: Alzheimer's Association Session Announced. Learn how lifestyle interventions can reduce the risk of cognitive impairment, how blood-based biomarkers are enabling earlier, more accessible Alzheimer’s diagnosis and advancements in treatments. The second half of this session will provide a comprehensive overview of rapidly moving innovations within dementia care specialty models including both Medicare and Medicare Advantage funded approaches. Be sure to add this Wednesday morning session to your plans!” *** STC GAINS ACCEPTANCE as Dennis Rinner of GoldenCareUSA explains in this article that we highlighted in the following LTC Clipping last week. LTC Clippings are a daily feature we bring to Center for LTC Reform premium members. Steve Moses tracks the news and analysis bearing on LTC issues of all kinds. He cites the source, pulls a representative quote, and gives his interpretation of important articles, reports, and news items. To join the Center and get access to our LTC Clippings, LTC Bullets, LTC E-Alerts and our members-only website, go to https://centerltc.com/support/index.htm or contact Damon at 206-283-7036 or damon@centerltc.com. 10/30/2025, “7 ESSENTIALS in every Short-Term Care (Extended Care) & Home Health Care Plan,” by Dennis Rinner, GoldenCareUSA Quote: “In the last couple years, there has been a major paradigm shift in the extended care product space: The landscape is changing. Agents and consumers (in particular, seniors) are aligned in demanding products that are more consumer and senior friendly. Everyone wants: 1. Less Underwriting … 2. Less Complicated … 3. Less Costly …Shorter-duration plans can be more flexible, are significantly lower in cost (more affordable than LTC alternatives), but they can still be comprehensive in the amount of coverage clients can select. … Let’s take a closer look at these seven essentials:

LTC

Comment: Click through for all the details in this excellent review

of the new world of extended care coverage. Dennis Rinner has the real

world experience and GoldenCareUSA has the wide reach to support agents

and consumers in the STC and LTC space throughout the country. *** LTC BULLET: THE $97 TRILLION LTC PARADOX LTC Comment: Last January I had this insight. The United States government encourages Americans to save and invest. Public policy rewards putting money aside for retirement, building home equity, and amassing life insurance cash value. But the same government’s policies—ironically and counterintuitively—discourage spending that accumulated wealth for high-quality private long-term care. As a result, most Americans who face elevated LTC expenditures end up on Medicaid, a means-tested public welfare program. How can that be, I wondered. What are the consequences for care access and quality? Could different policies make better use of America’s vast wealth to improve its dysfunctional LTC system? That puzzle and those questions led me to draft the following paper. It became the basis for a vastly revised “Policy Analysis” titled “Better Long-Term Care for Billions Less,” published November 13, 2025 by the Cato Institute. Because the piece published by Cato is very different from the original draft, focusing mostly on different points, I want to make the original available to LTC Bullets readers. Here it is. “The $97

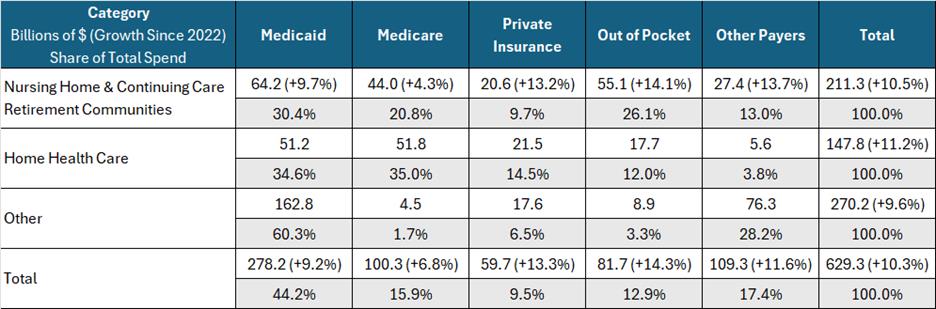

Trillion LTC Paradox” Executive Summary Government motivates personal asset accumulation with generous tax incentives. But it discourages spending the amassed wealth on long-term care (LTC), the single biggest financial risk aging Americans face. This contradictory policy undercuts LTC service delivery by relying too heavily on inadequate public financing. Resolving it in favor of more private LTC financing would reduce Medicaid expenditures by billions of dollars and simultaneously expand tax revenues from increased commercial activity. This paper explains why and how. Contradictory Policies Many government laws and regulations encourage private wealth accumulation in retirement savings, home equity, and life insurance. Tax-favored programs like IRAs and 401(k)s reward people for setting aside retirement funds. The federal government promotes home ownership with subsidized mortgages (FHA, VA, USDA), mortgage-interest tax deductions, and down payment assistance, enabling owners to grow equity. Life insurance receives favorable treatment through tax-deferred growth of cash value and tax-free death benefits. Thanks to these policies, Americans hold trillions of dollars in retirement savings ($40T),[1] home equity ($35T),[2] and life insurance ($22T),[3] $97 trillion in total for these resources alone. But little of this enormous wealth goes to pay for the potentially catastrophic cost of LTC. How can that be? LTC includes the long-term services and supports people require when they cannot perform basic activities of daily living without assistance. Such assistance may be needed due to injury, illness, frailty, cognitive impairment or old age. The need grows exponentially as America’s vulnerable aging population surges. Most of what we read about LTC in the popular and academic literature presumes that people all across the country are spending huge sums of money on nursing homes, assisted living facilities, and long-term home care. See for example the “Dying Broke” series by the New York Times and KFF.[4] The media tell us that many people spend down their life’s savings for this commonplace, unavoidable and supposedly uncompensated expense. In truth, the most reliable evidence shows that widespread, ruinous LTC spend down does not occur. What really happens? LTC Financing As the following table shows, government paid for most of the $629 billion America spent on LTC in 2023. Medicaid covered 44 percent and Medicare, 16 percent. Private insurance paid nine percent and other public and private sources, 17 percent. Thus, third parties covered the vast majority of all LTC expenses, 87 percent. Personal out-of-pocket spending (OOP) accounted for only 13 percent. As explained below, half of OOP came from income contributed mandatorily by people already on Medicaid, not from personal assets. Only six or seven percent of the entire cost of LTC could possibly come from spend down of private savings. At roughly $40 billion, out-of-pocket asset spend down barely nicks the tip of the nearly $100 trillion private wealth iceberg. Source: National Health Expenditures* Table: 2023 Total LTC Spending by Type and Source in Billions of Dollars with the Percentage Increase Since 2022[5]

* For definitions of all National Health Expenditure Accounts (NHEA) categories, see http://www.cms.gov/NationalHealthExpendData/downloads/quickref.pdf. How can it be that private wealth is largely off the table for financing LTC? For one thing, paid LTC services are far less common than many believe. Fifty-five percent of people who reach age 65 will not require any paid LTC. Thirty-one percent will need two years or less.[6] Those shorter term needs do fall largely on the public, but they are manageable. Johnson and Wang found that “Nearly nine in ten older adults have enough resources, including income and wealth, to cover assisted living expenses for two years.”[7] It is the remaining 14 percent of paid LTC lasting two years or more, especially the 4 percent lasting over five years, that incur crushing outlays due to the high cost of care. Median rates for nursing homes are $320 per day for a private room and $285 for a semi-private room; assisted living runs $5,350 per month; homemaker and home health aide services, $30 and $33 per hour, respectively.[8] Paid LTC need lasting for long periods at those high rates is clearly unaffordable by a public largely uninsured privately for the risk. So, as there is no evidence of widespread catastrophic private LTC spend down, we must focus on who or what pays instead and how exactly the public avoids this huge liability. Medicaid’s LTC Financing Role Medicaid pays for most of the longest, most expensive LTC needs. However, the public welfare program’s 44 percent share ($278 billion) of total 2023 LTC expenditures ($629 billion) understates its full impact on the service delivery system. Medicaid recipients are required to contribute most of their personal income (upwards of half of OOP), including their Social Security benefits (41% of OOP), to offset Medicaid’s cost for their care.[9] This supplemental private revenue makes the cost of Medicaid look smaller and out-of-pocket expenditures appear higher. After co-opting their private revenue in this way, Medicaid underpays LTC providers, reimbursing them on average only 70 percent of the rates they would otherwise have received from private payers.[10] The combined impact of Medicaid’s commandeering half of total out-of-pocket LTC spending, approximately $40 billion worth of private income, and then paying LTC providers often less than the cost of supplying the care[11] has had a devastating impact on LTC access and quality. Resulting meager wages worsen the nationwide shortage of paid caregivers. By dominating LTC financing while paying sub-market rates, Medicaid also shifts costs to a dwindling number of private payers who must pay higher rates for their usually shorter LTC terms of need to compensate. Thus, Medicaid is the dominant payer for the longest needs and largest LTC expenditures. But Medicaid is a public assistance program presumed to have draconian income and asset limits that block eligibility. That is why most analysts and the media assume that people must spend down both their income and assets for LTC until, impoverished, they qualify for Medicaid benefits. It is this “Fallacy of Impoverishment”[12] that resolves the paradox of low public out-of-pocket LTC spending despite sky-high national LTC expenditures. Financial Eligibility for Medicaid LTC Medicaid does require low income to qualify for LTC benefits, but most state Medicaid programs deduct private health and LTC expenditures from income before applying the low-income standard. So, even high income people qualify if their medical and LTC costs are commensurately high, as they usually are for seniors in need of expensive, extended care. Some states do cap income instead, but they allow special income diversion trusts to achieve the same purpose of enabling higher income people to qualify. Likewise, high assets do not interfere with eligibility for Medicaid LTC. Most large assets seniors own, such as homes, tax-favored retirement savings, or an automobile are exempt. Countable assets, such as cash, stocks, bonds, really anything easily convertible to cash, are usually capped at $2,000. But excess countable wealth is easily converted to exempt status by using it to purchase exempt assets. See “Medicaid’s $100+ Billion Leak.”[13] Long lists of exempt resources to facilitate this process are readily available on line or from financial advisers who specialize in reconfiguring clients’ income and assets to qualify them for Medicaid LTC benefits. Bottom line, virtually no amount of income or assets automatically disqualifies someone from qualifying for LTC funded by Medicaid and practically any amount of wealth can be reconfigured to secure Medicaid LTC eligibility. Mystery Solved It should be clear now what is going on. The conundrum of how private out-of-pocket LTC spending can be so low when total national LTC spending is so high is solved. The public handles relatively small, shorter-term LTC expenses out of their available income and assets without severe difficulty. But as LTC need extends in time and cost, pressure builds on families to find a way to fund the care. Millions take on the responsibility of caring for loved ones without pay, but the financial and emotional stress is so great that many seek help elsewhere. Turned away by Social Security and Medicare, which do not pay directly for LTC, they eventually discover Medicaid. There they find the help they seek, but it comes with all the downsides associated with the program such as the need to rejigger income and assets to qualify, access and quality problems, institutional bias, long home care waiting lists, and discrimination due to providers preferring higher-rate private payers. Consequences What are the ramifications of this unwieldy LTC system for each of its economic stakeholders? For government, the dominant payer, LTC is a huge expense that unrelentingly compounds budget deficits and long-term debt. For the public, LTC is a risk about which they are in denial until they need it, at which time Medicaid obviates the biggest cost, further desensitizing future generations to LTC risk. For senior advocates, LTC means seeking extra government benefits, while missing the irony that the more government spends on LTC, the less incentive people have to prepare privately for the risk. For Medicaid planners, LTC generates big profits from artificially impoverishing affluent clients to qualify them for benefits while holding back “key money” so their clients can access the best publicly financed care available to the exclusion of needier recipients. For care providers, LTC is a race for survival, as they struggle to supply quality care despite inadequate reimbursement from public programs that crowd out private payers at market rates. To the financiers who supply the debt and equity capital to build, operate and maintain care facilities, LTC requires a constant search to find profitable projects in a market dominated by poor public payers. Finally, for insurers, LTC is a hopeless challenge to sell a product government has been giving away since Medicaid began in 1965. These players in the LTC marketplace compete to squeeze scraps of benefit or profit from a centrally planned, government-dominated system that serves none of them well, and simultaneously defies reform. Solutions What can be done? This entrenched LTC economic system must be disrupted to its core. All payers, including Medicaid, should pay market rates to all LTC providers. This would reduce caregiver shortages and mitigate access and quality problems through market competition. To be able to pay market rates, however, Medicaid would need to cover fewer recipients. To reduce Medicaid LTC dependency without harming people in need, the program’s financial eligibility limits must be tightened gradually so that the public has time to adjust to a new reality of heightened private LTC risk. To achieve that objective, the system should exempt everyone under 55 years of age and anyone already needing LTC from the following changes. 1. Keep Medicaid’s treatment of income the same, continuing to require a low income standard after deducting private medical and LTC expenses from total income. Excess Social Security, pension and other private income should continue to offset Medicaid’s cost for recipients’ care, but the income flowing to LTC providers should be at market rates eliminating Medicaid’s artificially low reimbursements and reinvigorating the entire LTC service delivery system. 2. Stanch Medicaid’s $100+ Billion Leak. Stop allowing Medicaid applicants to purchase exempt assets in order to spend down unlimited, otherwise countable resources artificially. Instead, treat asset spend down the same as income spend down, by limiting it to deductions for actual, documented private medical or LTC expenditures. 3. Bring seniors’ $14 trillion[14] of home equity into the LTC financing system by eliminating or vastly reducing Medicaid’s home equity exemption. At its current 2025 level between $730,000 and $1,097,000,[15] Medicaid’s misplaced generosity diverts nearly all home equity away from LTC funding, enough alone to solve most of LTC’s many access and quality problems. 4. Stop “Medicaid Asset Protection Trusts”[16] and “Medicaid Compliant Annuities”[17] from diverting vast sums of private wealth from LTC spending into taxpayer-financed Medicaid expenditures. These legal gimmicks, used exclusively by the affluent clients of Medicaid planning specialists, should be illegal. 5. Medicaid’s 5-year asset transfer look-back[18] is too short to discourage intentional self-impoverishment to qualify for LTC benefits. Expand it to 20 years. As home ownership and transfers are publicly recorded by county assessors and recorders, respectively, a 20-year look-back rule could be easily administered. It would end one of the most commonly recommended early LTC planning methods. 6. End systemic LTC racism.[19] Today, affluent Medicaid planners’ clients access the best Medicaid facilities and services to the exclusion of needier groups, including racial and socio-economic minorities, by using “key money”[20] to purchase red-carpet LTC access that the less privileged cannot afford. When all funders, including Medicaid, pay market rates for care this unfair advantage benefiting the well-to-do over the underprivileged will disappear. 7. Give Medicaid back to the vulnerable aged and disabled people for whom it was originally intended by reversing the program’s new focus on able-bodied, working-age adults.[21] 8. Allow states to experiment with creative ways to do more with less by encouraging and approving waivers that trade federal matching fund limits for more state-level LTC policy flexibility. Implementing these eight measures will vastly reduce Medicaid LTC caseloads over time, including the most expensive cases dually eligible for Medicare and Medicaid. The new program will be better for all who qualify because it will pay market reimbursement rates adequate to ensure access to and quality of care across the care continuum from home to nursing home care. Middle class and affluent people no longer able to qualify for Medicaid LTC while sheltering wealth will find private pay LTC of higher quality and greater availability. They will pay market rates instead of higher private rates inflated by cost shifting caused by earlier artificially low Medicaid rates. With enormous sums of new private financing flowing through the LTC service delivery system at market rates, commercial activity will flourish generating additional tax revenue as more caregivers and LTC providers join the newly profitable sector. Obstacles This is an attractive picture. But getting from the dysfunctional system we have now to this vastly different organization of incentives and results is a problem. Critics will excoriate this new approach as uncaring toward people in need despite the irony that most of them believe incorrectly that the existing LTC system already impoverishes millions. But in truth this change will mean better LTC for those most in need who will continue to qualify for assistance from Medicaid. Others who become responsible to pay for their own LTC before they qualify for Medicaid will have time to adjust and prepare before they are affected. People already in need of LTC or under age 55 will remain unaffected and covered by Medicaid. The biggest challenge to re-inventing LTC in this way is how to awaken the public to the new reality without inciting opposition. No longer will people be able to ignore the risk and cost of LTC in their younger years and still receive Medicaid LTC in old age while preserving wealth. How to achieve a transition from current LTC complacency and government dependency to serious personal responsibility and planning is the major obstacle. Families struggling to make ends meet and save for their own retirement will not look kindly at a new obligation to save, invest or insure for LTC. How can they be relieved of that burden while simultaneously reducing the public financing option that has failed everyone so miserably? Answers The solution is to re-prioritize LTC among life’s responsibilities. As this paper has explained, public policy rewards the accumulation of savings, but discourages the use of private wealth to fund LTC. Why should amassing wealth that will pass to heirs if unspent take precedence over funding quality LTC for the living? Why should Medicaid incentivize heirs to use welfare-financed care for their infirm parents’ LTC needs? What if public policy prioritized preparing privately for future LTC need instead? What might such policy look like? Step one is to inform the public about the loss of Medicaid as a late-life wealth preserving safety net for the middle class and affluent. Then establish and promulgate new LTC planning goals for consumers to achieve no later than age 65 as a precondition for any later Medicaid help with catastrophic costs. Give every citizen an objective analysis of their LTC risk and an estimate of the likely cost of the care they may need some day. Each person could then know what they need to set aside to cover their average expected LTC need. Research shows that an overall average is $70,000 invested by age 65 will cover median paid LTC need.[22] Of course individuals may need to set aside less or more depending on their unique circumstances. While ensuring that every individual’s average LTC risk is covered by private funding would not eliminate Medicaid’s back end catastrophic risk, it would substantially reduce that risk enabling Medicaid to do a better job for all remaining long-duration recipients. How can people achieve their needed level of LTC savings without undue pressure on their ongoing living needs? One way could be to allow or require individuals and families to earmark other resources they are accumulating, such as retirement savings, home equity or life insurance, to be used for LTC if and only if otherwise unaffordable LTC needs occur in the future. In that manner, wealth being accumulated with strong public policy inducements can be repurposed to fund future LTC without impairing families’ current cash flow. Savings that would otherwise pass through inheritance would go to fund higher quality LTC for the living and create a stronger inducement for younger generations to save, invest or insure for their own future LTC need. Conclusion Some government policies encourage citizens to accumulate vast savings. But other public policies discourage them from spending this wealth on LTC. Easy access to Medicaid LTC benefits late in life enables people to ignore LTC risk and cost when they are young without drastic financial consequences later. As a result, few people plan, save, invest or insure for LTC early in life and they end up dependent on Medicaid late in life. But Medicaid distorts the LTC market by dominating it, paying too little for care, and thus causing caregiver shortages and other access and quality problems. To fix LTC, all payers, including Medicaid, should pay market rates enabling competition to ameliorate service delivery and financing problems. For Medicaid to pay market rates, however, LTC caseloads must decline dramatically. To reduce LTC caseloads, tighten Medicaid LTC financial eligibility limits by ensuring that recipients actually spend down income and assets for real private medical and LTC expenses before becoming eligible. To prepare the general public for this less easily available Medicaid LTC program, identify each person’s likely LTC risk and cost, then let them earmark enough from assets they are otherwise accumulating to satisfy their LTC planning responsibility if and only if needed to fund their future LTC. This

arrangement will induce people to plan for LTC earlier and to pay

privately for their care when needed. That private spending will reduce

the cost of LTC for Medicaid. Medicaid, relieved of covering so many

people who should, could and would have paid for their own LTC absent

current public policy incentives to the contrary, will be able to do a

better job for all remaining, genuinely needy recipients. The terrible

condition of LTC service delivery and financing in the United States is

not the result of too little government funding and regulation, but too

much. Reconfiguring the carrots and sticks in public policy to redirect

vast personal savings toward private LTC financing is the key to improve

LTC for everyone, rich and poor alike. [1] Natalie Lin, “US Retirement Assets Hit Record $40T,” Plan Advisor, September 20, 2024, https://www.planadviser.com/us-retirement-assets-hit-record-40t/ [2] Keith Griffith, “Homeowners Are Sitting on Their Biggest Share of Equity Since the 1950s,” realtor.com, October 1, 2024, URL: “Meanwhile, aggregate homeowner equity reached a new high of $35.1 trillion for the quarter, up 10% from a year ago and triple what it was 10 years ago.” [3] American Council of Life Insurers, 2024 Life Insurers Fact Book, November 8, 2024, [LINK]: “By the end of 2023, total life insurance coverage in the United States was $22.2 trillion, an increase of 1.6 percent from 2022 (Table 7.1).” [4] KFF, “Dying Broke: A New Jointly Reported Series on America’s Long-Term Care Crisis from KFF Health News and The New York Times,” November 14, 2023, KFF Health News, [LINK] [5] Note that KFF argues that Medicare and Private Insurance should not be included in LTC expenditures, which would drop the total for 2023 from $629.3 billion to $469.3 billion, raise Medicaid’s share from 44.2 percent to 59.3 percent and increase out-of-pocket expenditures from 12.9 percent to 17.4 percent. I disagree with KFF’s reasoning. For their analysis and mine, see respectively Priya Chidambaram and Alice Burns, “10 Things About Long-Term Services and Supports (LTSS),” KFF, July 8, 2024 [LINK] and Stephen A. Moses, “LTC Bullet: LTC Data Manipulation,” Center for Long-Term Care Reform, August 30, 2024, https://centerltc.com/bullets/archives2024/1388.htm [6] Richard W. Johnson and Judith Dey, “Long-Term Services and Supports for Older Americans: Risks and Financing, 2022,” ASPE Research Brief, August 2022 (Revised), p. 6, [LINK] [7] Richard W. Johnson and Claire Xiaozhi Wang, “The Financial Burden of Paid Home Care on Older Adults: Oldest and Sickest Are Least Likely to Have Enough Income,” Health Affairs, 38, No. 6 (2019), p. 1000, https://www.healthaffairs.org/doi/10.1377/hlthaff.2019.00025 [8] Genworth Cost of Care Survey 2023, Genworth Financial, Inc., July 11, 2024, https://pro.genworth.com/riiproweb/productinfo/pdf/131168.pdf [9] Recent academic LTC literature does not distinguish between the share of out-of-pocket LTC expenditures coming from personal income as opposed to assets or savings. We know from earlier analysis, however, that it is substantial. According to Lazenby and Letsch (1989): “An estimated 41 percent … of out-of-pocket spending for nursing home care was received as income by patients or their representatives from monthly social security benefits ... .” Given that elderly people have other sources of income besides Social Security, such as pensions, annuities and investment returns, all of which, except for a small monthly maintenance needs allowance, must be contributed to offset Medicaid’s cost for their care, it is reasonable to assume that income, as opposed to asset spend down, approaches or exceeds 50 percent of total out-of-pocket LTC spending. Helen C Lazenby, Suzanne W Letsch, “National health expenditures, 1989,” Health Care Financing Review, 1990 Winter;12(2):1–26, [LINK] [10] American Council on Aging. “2021 Nursing Home Costs by State and Region, Understanding the Difference Between Private Pay and Medicaid Reimbursement,” https://www.medicaidplanningassistance.org/nursing-home-costs. Accessed January 4, 2025. [11] Liz Liberman, “Medicaid Reimbursement Rates Draw Attention,” NIC/CARES blog, 2018, https://www.nic.org/blog/medicaid-reimbursement-rates-draw-attention/ [12] Stephen A. Moses. “The Fallacy of Impoverishment,” The Gerontologist, volume 30, Issue 1, February 1990, pages 21–25, https://academic.oup.com/gerontologist/article-abstract/30/1/21/586769 [13] Stephen A. Moses, “Medicaid’s $100+ Billion Leak,” Paragon Health Institute, July 1, 2024, https://paragoninstitute.org/paragon-prognosis/medicaids-100-billion-leak/ [14] Erica Drzewiecki, “Senior Home Equity Reaches $14 Trillion,” National Mortgage Professional, October 8, 2024, URL. [15] American Council on Aging, “Projected 2025 Medicaid Long-Term Care Financial Eligibility Criteria: Home Equity Limits,” accessed January 4, 2025, https://www.medicaidplanningassistance.org/medicaid-eligibility-2025/ “States projected to use $1,097,000 as the home equity limit in 2025: Colorado, Connecticut, District of Columbia, Hawaii, Massachusetts, New Jersey, New York, and Washington. … California does not have a home equity limit.” [16] American Council on Aging, “How Medicaid Planning Trusts Protect Assets and Homes from Estate Recovery,” accessed January 4, 2025, https://www.medicaidplanningassistance.org/asset-protection-trusts/ [17] American Council on Aging, “How Purchasing a Medicaid Compliant Annuity Impacts Eligibility for Medicaid Long-Term Care,” accessed January 4, 2025, https://www.medicaidplanningassistance.org/eligibility-by-annuity/ [18] American Council on Aging, “Understand Medicaid’s Look-Back Period; Penalties, Exceptions & State Variances,” accessed January 4, 2025, https://www.medicaidplanningassistance.org/medicaid-look-back-period/ [19] Tetyana Pylypiv Shippee, et al., “Evidence for Action: Addressing Systemic Racism Across Long-Term Services and Supports,” Journal of the American Medical Directors Association, February 2022, 23(2):214-219, https://pubmed.ncbi.nlm.nih.gov/34958742/ [20] Search for “key money” in this article: Flaster Greenberg PC, “Top Tips For A Successful Medicaid Spend Down,” May 17, 2019, accessed January 4, 2025, https://www.jdsupra.com/legalnews/top-tips-for-a-successful-medicaid-67619/ [21] Brian Blase, “Medicaid Financing Reform: Stopping Discrimination Against the Most Vulnerable,” Paragon Health Institute, July 24, 2024, URL. [22] Inferred from Johnson and Dey as explained in “Long-Term Care: The Solution,” p. 17, footnotes 47-50. |