|

ADS

Place your advertisement

here.

Email

info@centerltc.com

or call Damon at 206-283-7036 for advertising rates.

American Independent Marketing

Join the Center for Long-Te Care Reform.

Help us fight for rational LTC policy reform.

Receive our daily email publications.

Get a user name and password to our Members-Only Zone.

Only $150 per year.

Mail your check to Center for Long-Term Care Reform, Inc., 2212 Queen Anne

Avenue North, #110, Seattle, Washington, 98109.

Contact Damon at 206-283-7036 or

damon@centerltc.com

if you have questions. Join

the team!

|

READ STEVE'S BIO.JPG)

#############################

Updated Monday, August 10, 10:03 AM

(Pacific)

Seattle—

#############################

LTC

E-ALERT #26-028: LTC NEWS AND COMMENT

LTC

Comment: Do you spend hours searching the internet for useful articles,

key data, and relevant reports to keep you on the forefront of

professional knowledge? Do you lose business because you’re blindsided by

clients or competitors who learn critical information before you do?

Here’s an antidote:

LTC

Clippings: The Center for Long-Term Care Reform notifies subscribers to

our LTC Clippings service daily of information you need to know. Each

message contains only the critical facts about new publications: a title,

representative quote, a link to the original, and our analysis in a

sentence or two. To inquire or subscribe, contact Damon at 206-283-7036

or

damon@centerltc.com.

Read testimonials by satisfied subscribers

here.

To subscribe online, please click

here.

LTC

E-Alerts: Once a week, we compile our daily LTC Clippings into a summary,

email it to Center for Long-Term Care Reform members, and archive it in

The Zone, our password-protected members-only website. Center members

also receive our weekly LTC Bullet op-ed. To join the Center and receive

all these benefits and more, contact Damon at 206-283-7036 or

damon@centerltc.com.

We no

longer post our LTC E-Alerts on the Center’s public access website, but

here’s what today’s LTC E-Alert contained: links, quotes and comments on

the following articles, reports, or data:

-

CareScout Redefines Worksite Long-Term Care

Insurance With a Solution That Goes Further for Employers and Employees

-

Senior care and living sector outperforms others in

real estate for seventh quarter in a row

-

Providers tap new AI tools to minimize managed care

requests and denials

-

The Facts About Medicare Spending

-

How CMS Can Restore Program Integrity to Medicaid

by Eliminating Passive Redetermination Requirements

-

Lumos Insurance Introduces the Immediate Care Plan

to Help Families Fund Long-Term Care

-

Can You Actually Get Paid to Care for an Aging

Parent?

-

Ownership changes, regulatory and reimbursement

pressures top reasons for nursing home closures, study finds

#############################

"LTC E-Alerts" are

a feature

offered by the Center for Long-Term Care Reform, Inc. to members at the

$150 per year level or higher. We'll track and report to you news and

analysis regarding long-term care financing, service delivery, and

research. We hope The LTC E-Alerts will help you attain and maintain a

high level of knowledge and competency in this complex field. The

Center for Long-Term Care Reform, Inc. is a private institute dedicated to

ensuring quality LTC for all Americans (www.centerltc.com).

#############################

Updated Friday, August 7, 2026, 10:03 AM (Pacific)

Seattle—

#############################

LTC BULLET: PARAGON ON

MEDICAID AND LONG-TERM CARE

LTC Comment:

Paragon Health Institute, America’s

leading health policy think tank, brought Medicaid and LTC inequities to

the Senate Budget Committee’s attention this week. The

hearing video is captivating. We

elaborate after the ***news.***

*** 8/4/2026, “Lumos

Insurance Introduces the Immediate Care Plan to Help Families Fund

Long-Term Care,” StreetInsider.com

Quote:

“Lumos

Insurance™ today announced the general

availability* of its Immediate

Care Plan, a fully underwritten single

premium immediate annuity built for people who already need paid care. A

single lump sum is exchanged for guaranteed monthly income for life, with

payments beginning within one month, so families can fund an assisted

living community, a memory care unit, or in-home care without drawing down

every other asset they have. … The Immediate Care Plan addresses what

Lumos calls the Care Gap: the recurring difference between the monthly

cost of formal care and the income a family already has coming in

from Social Security, a pension, or other sources. … ‘The Care Gap is

showing up in advisors' offices every week, and without a solution, it can

put a lifetime of savings at risk,’ said Vince Bodnar, President of Lumos

Insurance and a two-time chairperson of the Society of

Actuaries' Long-Term Care Insurance Section. ‘When a product is priced for

the average person instead of the individual, families may commit more

assets than their situation requires. The families arriving at the care

transition today deserve solutions built for their actual circumstances —

not actuarial averages. Lumos is excited to offer our Immediate Care Plan

to help meet this need.’”

LTC Comment:

Congratulations to Center-corporate-member Lumos and its president Vince

Bodnar on the introduction of this promising new solution to a

longstanding problem for LTC consumers. ***

LTC BULLET: PARAGON ON

MEDICAID AND LONG-TERM CARE

LTC Comment: Paragon

president Brian Blase described the hearing and his testimony in the

Institute’s

weekly newsletter:

“Medicaid:

The Reality” was the first Senate Budget

Committee hearing under Chairman Ron Johnson’s leadership. My oral

testimony focused on Medicaid’s

fundamentally broken financing incentives. I explained that the ACA

created a financing formula that pays states roughly $9 in federal funds

for every $1 they spend on able-bodied, working-age Medicaid expansion

adults, compared to an average of $1.33 for every $1 spent on traditional

enrollees. That sevenfold disparity encourages states to prioritize

expansion adults over the populations Medicaid was originally created to

serve—and has resulted in worse health care access for traditional

enrollees. I also described how provider taxes, state-directed payments,

and other financing arrangements have evolved into a legalized Medicaid

money-laundering apparatus that shifts costs from states to federal

taxpayers while generating tens of billions of dollars in corporate

welfare for politically powerful providers, insurers, and consultants.”

Do yourself a favor and

watch this video of the full hearing: “Medicaid:

The Reality” . It is engaging and

informative, but for pure entertainment value, check out

the exchange between Senator John Kennedy and Brian Blase.

Also of interest, testimony by Jonathan Ingram, Vice President of Policy

and Research at the Foundation for Government Accountability, concerning

Medicaid’s excessive improper payments. The third witness at the hearing,

Mr. Andy Schneider,

Research Professor of the Practice Center for Children and Families,

McCourt School of Public Policy, Georgetown University, is a study in

hapless defense of Medicaid’s dysfunctions in the face of hard, empirical

evidence of their damage.

But you might ask: What

does this have to do with long-term care? ObamaCare’s (ACA’s) expansion

population generates 90% federal matching funds for state Medicaid

programs when they cover able-bodied, working age adults. At seven times

the match for poor women, children, the aged, blind and disabled (ABD),

this distorted incentive moved Medicaid funding away from the program’s

traditional, more vulnerable enrollees. For example, ABD recipients were a

quarter of total enrollment in 2010 (when the ACA passed) and they

consumed nearly 2/3 of all Medicaid expenditures. By 2025, ABD recipients

were down to 1/5 of total enrollments and they accounted for only half of

total expenditures. This ABD population consumes the majority of LTC

benefits—including nursing facility care and home and community-based

services (HCBS). LTC alone accounts for approximately one-third (30% to

33%) of all Medicaid spending, despite being used by only 6% of total

Medicaid recipients who are mostly ABD. Prioritizing able-bodied, working

age adults over Medicaid’s original target population of those most

vulnerable and in need has changed the program’s focus from helping those

with the greatest need into a non-tax federal money generator for states.

More on Long-Term

Care

Congressional hearing

testimony generally takes the form of brief verbal statements by witnesses

who also submit much more detailed written testimony. Most interesting to

us is that Brian Blase’s written testimony included the following content

close to our hearts. By highlighting the problem of excessive use of

Medicaid LTC by people who could, should and would have paid their own way

and stayed off Medicaid, Blase pointed the way toward better policy to

benefit both the poor and the more affluent.

The following is a quote

from Brian Blase’s

written testimony:

“MEDICAID’S DAMAGE TO

RESPONSIBLE LONG-TERM CARE PLANNING

“A fundamental flaw in

America’s long-term care system is that Medicaid has evolved from a safety

net for the poor into an inheritance protection program for many

households with substantial assets. Through generous asset exemptions,

home equity exclusions, trusts, and estate-planning strategies, many

individuals can qualify for taxpayer-financed long-term care while

preserving significant wealth for their heirs. Rather than requiring

families to use accumulated assets to finance their own care before

relying on public assistance, current policy often allows Medicaid to pay

first while inheritances remain largely intact. This is inequitable to

taxpayers who save responsibly and distorts the program’s original

purpose.

“These policies also

create powerful disincentives for individuals to prepare for their own

long-term care needs. When people expect Medicaid to cover nursing home

costs or home-based care after modest planning or asset restructuring,

they have less reason to purchase long-term care insurance, accumulate

dedicated savings, or otherwise plan for a predictable risk associated

with aging. The result is a classic moral hazard: private financing

declines because public financing is readily available. As more people

rely on Medicaid, the program consumes more taxpayer resources while

providers become increasingly dependent on low Medicaid reimbursement

rates, contributing to workforce shortages, limited access to high-quality

care, and persistent financial pressures throughout the long-term care

system.68

“The irony is that these

policies often harm the very people they are intended to help. By

encouraging reliance on Medicaid rather than personal planning, they

weaken the market for private long-term care financing and reduce the

resources available to improve care quality for the most vulnerable. A

system that requires individuals with sufficient means to finance more of

their own long-term care before turning to Medicaid would better preserve

the program for those with genuine financial need while encouraging

greater personal responsibility and a stronger private market for

long-term care services.

“III. Recommendations

to Improve the Medicaid Program …

“Reform

Medicaid long-term care

“Medicaid should not be

used to preserve inheritances for wealthy heirs. Congress should ensure

that people with sizeable assets are not able to use Medicaid to finance

their long-term care expenses.

“These reforms will

reduce waste, fraud and abuse and provide Medicaid a responsible fiscal

trajectory to ensure we continue to have the ability to care for our most

vulnerable.”

68

Stephen Moses, "Long-Term Care: The Problem," Paragon Health Institute,

October 2022, https://paragoninstitute.org/medicaid/long-term-care-problem/

LTC Comment:

My role as a

Visiting Fellow with the

Paragon Health Institute has widened the

reach of the Center for LTC Reform’s research and analysis through

numerous reports and articles for

Paragon.

#############################

Updated

Monday, August 3, 10:03 AM (Pacific)

Seattle—

#############################

LTC E-ALERT #26-027:

LTC NEWS AND COMMENT

LTC Comment: Do you

spend hours searching the internet for useful articles, key data, and

relevant reports to keep you on the forefront of professional knowledge?

Do you lose business because you’re blindsided by clients or competitors

who learn critical information before you do? Here’s an antidote:

LTC Clippings: The

Center for Long-Term Care Reform notifies subscribers to our LTC Clippings

service daily of information you need to know. Each message contains only

the critical facts about new publications: a title, representative quote,

a link to the original, and our analysis in a sentence or two. To inquire

or subscribe, contact Damon at 206-283-7036 or

damon@centerltc.com.

Read testimonials by satisfied subscribers

here.

To subscribe online, please click

here.

LTC E-Alerts: Once a

week, we compile our daily LTC Clippings into a summary, email it to

Center for Long-Term Care Reform members, and archive it in The Zone, our

password-protected members-only website. Center members also receive our

weekly LTC Bullet op-ed. To join the Center and receive all these

benefits and more, contact Damon at 206-283-7036 or

damon@centerltc.com.

We no longer post our

LTC E-Alerts on the Center’s public access website, but here’s what

today’s LTC E-Alert contained: links, quotes and comments on the

following articles, reports, or data:

-

How to make social

care sustainable

-

Federal Government

Spending Is a Leaky Bucket

-

New resource helps

senior living professionals share sector’s value proposition over

staying at home

-

The Retirement

Myth Everyone Gets Wrong About Medicare

-

The Medicaid Rule

That Can Put Your Family Home at Risk

-

Retirement-long

medical expenses increasing for older adults, cutting into savings

-

How Much Would A

Public Long-Term Care Insurance Program Cost?

-

As the cost of

aging soars, families’ wealth is evaporating

#############################

"LTC E-Alerts" are

a

feature offered by the Center for Long-Term Care Reform, Inc. to members

at the $150 per year level or higher. We'll track and report to you news

and analysis regarding long-term care financing, service delivery, and

research. We hope The LTC E-Alerts will help you attain and maintain a

high level of knowledge and competency in this complex field. The

Center for Long-Term Care Reform, Inc. is a private institute dedicated to

ensuring quality LTC for all Americans (www.centerltc.com).

#############################

Updated Monday, July 27, 10:03 AM

(Pacific)

Seattle—

#############################

LTC

E-ALERT #26-026: LTC NEWS AND COMMENT

LTC

Comment: Do you spend hours searching the internet for useful articles,

key data, and relevant reports to keep you on the forefront of

professional knowledge? Do you lose business because you’re blindsided by

clients or competitors who learn critical information before you do?

Here’s an antidote:

LTC

Clippings: The Center for Long-Term Care Reform notifies subscribers to

our LTC Clippings service daily of information you need to know. Each

message contains only the critical facts about new publications: a title,

representative quote, a link to the original, and our analysis in a

sentence or two. To inquire or subscribe, contact Damon at 206-283-7036

or

damon@centerltc.com.

Read testimonials by satisfied subscribers

here.

To subscribe online, please click

here.

LTC

E-Alerts: Once a week, we compile our daily LTC Clippings into a summary,

email it to Center for Long-Term Care Reform members, and archive it in

The Zone, our password-protected members-only website. Center members

also receive our weekly LTC Bullet op-ed. To join the Center and receive

all these benefits and more, contact Damon at 206-283-7036 or

damon@centerltc.com.

We no

longer post our LTC E-Alerts on the Center’s public access website, but

here’s what today’s LTC E-Alert contained: links, quotes and comments on

the following articles, reports, or data:

-

Kansas City won’t escape the US debt crisis. Here’s

what we must do now

-

The Average Net Worth of Americans at 85, And The 8

Assets Separating the Comfortable From the Struggling

-

Rewarding Reform, Punishing Neglect: How Annual

Improper Payment Reviews Can Fix Medicaid Accountability

-

Managed care plan’s termination of assisted living

program leaves providers in limbo

-

Caregiver Burnout — Why Generic Advice Fails and

What Works

-

Older adults’ home equity reaches a record $14.92T

in first quarter

-

BREAKING: New exclusion authority expected to be

‘force multiplier’ for CMS fraud enforcement

-

Despite DOJ policy shift, state obligations to

people with disabilities remain

-

SNF occupancy hits highest level in a decade: NIC

-

Spouses of patients with dementia nearly 75 percent

more likely to develop same condition, large study finds

#############################

"LTC E-Alerts" are

a feature

offered by the Center for Long-Term Care Reform, Inc. to members at the

$150 per year level or higher. We'll track and report to you news and

analysis regarding long-term care financing, service delivery, and

research. We hope The LTC E-Alerts will help you attain and maintain a

high level of knowledge and competency in this complex field. The

Center for Long-Term Care Reform, Inc. is a private institute dedicated to

ensuring quality LTC for all Americans (www.centerltc.com).

#############################

Updated Friday, July 24, 2026, 10:03 AM (Pacific)

Seattle—

#############################

LTC BULLET: LONG-TERM

CARE FRAUD

LTC Comment: LTC fraud

is large and growing especially in the public sector, which could learn

from the private sector’s better identification and control methods. We

announce a new Center report on LTC fraud, after the ***news.***

***

illumifin, the leading insurance third party administrator (TPA) and

longtime Center-corporate member, inspired and assisted our work on LTC

insurance fraud. The company’s excellent presentations on LTCI fraud at

the 2025 Intercompany LTC Insurance Conference last March pointed the

direction for our research. Executive Chairman Peter Goldstein encouraged

our study and Jeffrey Ferrand, Vice President of Fraud Services at

illumifin, provided helpful advice and suggestions. We thank the company

and its officials for the path-breaking work they’ve done to identify,

prevent, and prosecute the various forms of fraud confronting the

long-term care insurance industry. ***

LTC BULLET: LONG-TERM

CARE FRAUD

LTC Comment: Today, the

Center for Long-Term Care Reform published a new report titled “Long-Term

Care Fraud.” Its “Executive Summary” and “Conclusion” follow below but you

can check out the complete report

here.

Long-Term Care Fraud

by

Stephen A. Moses

July 23, 2026

Executive Summary

Health care fraud is

large already and growing rapidly. Long-term care (LTC), vital because of

America’s aging population, is especially susceptible to fraud. Government

or corporate third parties finance most LTC which creates a moral hazard

by facilitating fraud and reducing its risk. Individuals, naturally averse

to fraud, fund much less LTC out of their own pockets. Most LTC is

delivered in private homes without supervision inviting fraudulent

billings. We know the incidence and cost of fraud in private LTC

insurance. But there is no published measure of LTC fraud in the public

sector. Medicaid and Medicare present special problems that make LTC fraud

identification, processing and prosecution exceptionally difficult. The

Trump administration has undertaken a major push to reduce public sector

health care fraud. Private sector advances to control LTC fraud could help

reduce obstacles on the public side. A key is prioritization, focusing on

cases most likely to produce results. This paper examines LTC fraud in

both sectors and recommends measures to curtail its growth and impact.

…

Conclusion

LTC fraud is inevitable

in a health care system that relies heavily on third-party payment,

limited supervision, and complicated public administration. As demand for

LTC grows with population aging, the chances for phantom billing, upcoding,

identity abuse, and organized fraud expand unless payers respond more

aggressively. Private LTC insurers have identified and reduced fraud by

using targeted investigation, risk scoring, and early intervention instead

of waiting to recover losses after the fact. Public programs, especially

Medicaid and Medicare, face greater barriers, but they could employ the

most effective private-sector practices more aggressively. Focus on

high-risk claims; use data analytics to stop suspicious payments earlier;

and prioritize cases with the greatest return on investigative effort. In

a system where most LTC spending comes from third parties, fraud control

will always depend on incentives. Replacing Medicaid’s wide open federal

funds matching system with capped block grants would encourage states to

focus more vigorously on fraud control. Absent the temptation of unlimited

federal revenue, state Medicaid programs would more effectively protect

vulnerable recipients, preserve public funds, and maintain trust in

long-term care.

#############################

Updated

Monday, July 20, 10:03 AM (Pacific)

Seattle—

#############################

LTC E-ALERT #26-025: LTC NEWS AND COMMENT

LTC Comment: Do you spend hours searching

the internet for useful articles, key data, and relevant reports to keep

you on the forefront of professional knowledge? Do you lose business

because you’re blindsided by clients or competitors who learn critical

information before you do? Here’s an antidote:

LTC Clippings: The Center for Long-Term

Care Reform notifies subscribers to our LTC Clippings service daily of

information you need to know. Each message contains only the critical

facts about new publications: a title, representative quote, a link to

the original, and our analysis in a sentence or two. To inquire or

subscribe, contact Damon at 206-283-7036 or

damon@centerltc.com.

Read testimonials by satisfied subscribers

here.

To subscribe online, please click

here.

LTC E-Alerts: Once a week, we compile our

daily LTC Clippings into a summary, email it to Center for Long-Term Care

Reform members, and archive it in The Zone, our password-protected

members-only website. Center members also receive our weekly LTC Bullet

op-ed. To join the Center and receive all these benefits and more,

contact Damon at 206-283-7036 or

damon@centerltc.com.

We no longer post our LTC E-Alerts on the

Center’s public access website, but here’s what today’s LTC E-Alert

contained: links, quotes and comments on the following articles, reports,

or data:

-

HSAs undertapped

as way to save for long-term care, retirement needs, survey finds

-

Violence

repeatedly erupts in dementia care despite warnings, inspections show

-

My mom's long-term

care has cost almost $400,000. This is after we spent $45,000 converting

a guest house on our property for her

-

New study

quantifies the annual cost of dementia at $818 billion, with families

picking up most of the tab

-

[UPDATED] CMS to

reward higher-performing nursing homes with ‘streamlined’ reviews,

favorable online icon

-

Five Key Facts

About Spending and Enrollment for People with Medicare and Medicaid

(Dual-Eligible Individuals)

-

Report offers

roadmap for future-proofing care for older adults

-

Alzheimer’s

Association starts $100M trial to evaluate impact of GLP-1s on cognitive

decline

-

Baby boomers

retiring with record mortgage, credit card debt

-

Improving Access

to Medicare Home Health Care: Key Policy Considerations

#############################

"LTC E-Alerts" are

a

feature offered by the Center for Long-Term Care Reform, Inc. to members

at the $150 per year level or higher. We'll track and report to you news

and analysis regarding long-term care financing, service delivery, and

research. We hope The LTC E-Alerts will help you attain and maintain a

high level of knowledge and competency in this complex field. The

Center for Long-Term Care Reform, Inc. is a private institute dedicated to

ensuring quality LTC for all Americans (www.centerltc.com).

#############################

Updated

Monday, July 13, 10:03 AM (Pacific)

Seattle—

#############################

LTC E-ALERT #26-024: LTC NEWS AND COMMENT

LTC Comment: Do you spend hours searching

the internet for useful articles, key data, and relevant reports to keep

you on the forefront of professional knowledge? Do you lose business

because you’re blindsided by clients or competitors who learn critical

information before you do? Here’s an antidote:

LTC Clippings: The Center for Long-Term

Care Reform notifies subscribers to our LTC Clippings service daily of

information you need to know. Each message contains only the critical

facts about new publications: a title, representative quote, a link to

the original, and our analysis in a sentence or two. To inquire or

subscribe, contact Damon at 206-283-7036 or

damon@centerltc.com.

Read testimonials by satisfied subscribers

here.

To subscribe online, please click

here.

LTC E-Alerts: Once a week, we compile our

daily LTC Clippings into a summary, email it to Center for Long-Term Care

Reform members, and archive it in The Zone, our password-protected

members-only website. Center members also receive our weekly LTC Bullet

op-ed. To join the Center and receive all these benefits and more,

contact Damon at 206-283-7036 or

damon@centerltc.com.

We no longer post our LTC E-Alerts on the

Center’s public access website, but here’s what today’s LTC E-Alert

contained: links, quotes and comments on the following articles, reports,

or data:

-

A New Option for Long-Term Care Costs

-

US adult obesity rate rose from 30% to 41% between

1999 and 2023, study finds

-

It’s Time To Reform How The Federal Government

Funds State Medicaid Programs

-

Genworth CEO McInerney takes health leave as CFO

Upton steps in

-

New tool helps providers, others estimate how long

someone will be able to afford assisted living

-

Collateral damage: Medicaid work rules threaten

nursing homes even if patients keep coverage

-

The families we serve are becoming the workforce we

need

-

Long-Term and Assisted Care—Here’s What Medicare

and Medicaid Do and Do Not Cover

#############################

"LTC E-Alerts" are

a

feature offered by the Center for Long-Term Care Reform, Inc. to members

at the $150 per year level or higher. We'll track and report to you news

and analysis regarding long-term care financing, service delivery, and

research. We hope The LTC E-Alerts will help you attain and maintain a

high level of knowledge and competency in this complex field. The

Center for Long-Term Care Reform, Inc. is a private institute dedicated to

ensuring quality LTC for all Americans (www.centerltc.com).

#############################

Updated Friday, July 10, 2026, 10:03 AM (Pacific)

Seattle—

#############################

LTC Comment: If you

think LTC is in trouble now, wait until the rest of the boomers hit age 65

in 2029! We explain after the ***news.***

*** Did you see all of these important LTC stories

from the past few days? Probably not unless you track the industry media

and academic publications full time. That’s what Steve Moses does so he

can send these real time LTC Clippings to Center premium members

daily.

7/8/2026, “As

America Turns 250, It's Worth Celebrating Last Year's One Big Beautiful

Bill,” by Brian Blase, Paragon Health Institute

Quote: “Maximizing freedom requires limiting government. Last

year, Congress notched a win for freedom with the passage of the One Big

Beautiful Bill (OBBB), or the Working Families Tax Cut Act. Although the

cornerstone of the legislation was its provisions that lowered taxes, the

legislation also expanded freedom by taking steps to reduce the tide of

red ink emanating from federal health care programs, whose unsustainable

growth poses one of the greatest threats to America’s long-term

prosperity.”

LTC Comment: Have you seen the relentless media criticism of last

year’s budget reconciliation law? Read this excellent summary of the

OBBBA’s impact on government health care spending for a more accurate and

objective analysis.

7/7/2026, “The

Aging Population Is Changing States’ Revenue, Spending, and Service Demand

Outlook,” PEW

Quote: “The United States’ population is aging rapidly. And as

with other

long-term shifts in social and economic conditions, the transition to

an older population is already affecting state revenue and

expenditures. Understanding and preparing for these ongoing changes will

be critical to states’ future fiscal sustainability.”

LTC Comment: Read this report to learn now states are already in a

world of fiscal hurt due to population aging. Then contemplate how much

worse it will be without the ongoing federal Medicaid matching funds

bonanza as new limits on the use of provider taxes, intergovernmental

transfers, and state-directed payments take effect. No amount of planning

will shield states from what’s coming. Expect less government help for LTC,

not more.

If you’re not already a member of the Center for

Long-Term Care Reform, join

here. Check out our “Membership

Levels and Benefits” for all the individual and corporate membership

options. Join our campaign to ensure quality long-term care for all

Americans. ***

LTC BULLET: HOW MUCH

WORSE CAN LONG-TERM CARE GET?

LTC Comment: U.S.

long-term care (LTC) is in a world of hurt. The symptoms are well known:

access and quality problems, caregiver shortages, excessive reliance on

unpaid family caregivers, exploding public costs, and so on. Bad as it is,

however, evidence suggests it could, and likely will, get much worse.

Two articles in the

current issue of Health Affairs support that discouraging

conclusion. “National

Health Expenditure Projections, 2025–34: Strong Utilization Growth

Initially, Legislative Impacts Later”

tells us that the key components of LTC spending will grow annually on

average from 2025 to 2034 by the following percentages arriving at total

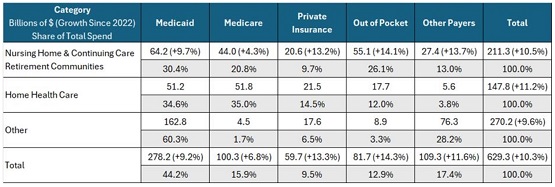

spending across all payers in billions of dollars as follows:

Nursing care facilities and

continuing care retirement communities:

4.4%, $338.3

Home health care:

8.1%, $367.8

Other health, residential, and personal

care: 6.7%, $615.0

OK, that’s bad enough

considering the 2024 numbers for the nursing homes, home health and other

categories were only $219.9, $169.4 and $320.5, respectively. But consider

how much worse LTC spending could get if the insights from the other

Health Affairs article are not adequately reflected in these

estimates.

According to “Trends

In Care Needs Among Older US Adults Diverged By Age, 2011–22,”

a new cohort of markedly more unhealthy baby boomers is about to throw

current expectations about LTC utilization and spending into a cocked hat.

For starters, consider

the status quo: “Nearly half of older adults in the United States

experience disability, often defined in later life as limitations with

daily activities … .” (p. 790) Half have ADL deficiencies? Already?

That’s alarming enough. But consider what’s coming according to the

“trends” article.

Among younger baby

boomers, “swelling numbers” are living with ADL limitations, receiving

paid care, and experiencing unmet care needs. Among older age groups,

however, there were declines in care received in all settings without

increases in unmet care needs. Overall, averaging the younger and older

cohorts, trends for the 65 and older population appeared stable with half

having ADL deficiencies.

But that current

stability is misleading. This study only analyzed the front half of the

baby boom generation. Future studies will address all the baby boomers and

will not be balanced by the better health and LTC characteristics among

the older cohort in the current study.

The trend article

authors conclude “the sizable rise in the numbers of adults ages 65–74

with activity limitations (an additional five and a half million),

receiving care (an additional three million), and with unmet care needs

(an additional two million) over a relatively short period is sobering.”

(p. 796)

“Sobering” is an

understatement. America’s over 85 age population will triple by 2050

dramatically increasing the number needing LTC. The article therefore

concludes:

Taken together, study

findings point to continued swelling in the numbers of older adults with

care needs as the second half of this generation reaches later life. They

also suggest that the share of older adults with care needs, which has

been flat for more than two decades, may soon begin to rise. (p. 796)

From its beginning in

1946, the baby boom generation dramatically transformed American society,

culture and economy. It’s about to shake up LTC services and spending

commensurately. The first tranche of baby boomers has more ADL

limitations, requires more paid care, and has more unmet LTC needs than

previous generations. Add in the younger boomers with LTC characteristics

as bad or worse and we can expect the LTC service delivery and funding

challenge to worsen radically.

So, what is to be done?

Do either of the Health Affairs articles offer helpful suggestions?

Alas, no. The projections article concludes “policy makers will

undoubtedly continue to explore options for addressing the significant

financing challenges for a sector that is expected to account for more

than one-fifth of the economy by 2034.” (p. 732) Want to hang our hopes on

policy makers finding a better funding source?

The trends article is no

more helpful. “Study findings reinforce the need for robust policies,

including innovations in workforce development and family supports, to

address the growing care needs of older adults and their families.” (p.

797) Where will the money come from to reinforce robust policies? That’s

typical doubletalk.

What these articles have

in common with most others of their ilk is that they analyze symptoms and

recommend solutions, but never ask why LTC is so dysfunctional in the

first place. With no idea of the source of LTC’s many problems, such

analysts have nowhere to go with their recommendations than to call for

more government spending and regulation.

For an entirely

different approach that addresses the cause of LTC problems first and then

proposes solutions, read the

Paragon Health Institute’s “Long-Term

Care: The Problem” and “Long-Term

Care: The Solution” and watch this “virtual

LTC event” featuring age wave visionary

Ken Dychtwald and leading LTC researchers. To find ample private funds for

LTC, check out “Medicaid’s

$100+ Billion Leak.” For what not to do,

see “Medi-Cal-amity:

California’s Reckless Expansion of Medicaid Long-Term Care to the Affluent.”

See also “Better

Long-Term Care for Billions Less.” Much

more on long-term care

here.

#############################

Updated

Monday, July 6, 10:03 AM (Pacific)

Seattle—

#############################

LTC E-ALERT #26-023: LTC NEWS AND COMMENT

LTC Comment: Do you spend hours searching

the internet for useful articles, key data, and relevant reports to keep

you on the forefront of professional knowledge? Do you lose business

because you’re blindsided by clients or competitors who learn critical

information before you do? Here’s an antidote:

LTC Clippings: The Center for Long-Term

Care Reform notifies subscribers to our LTC Clippings service daily of

information you need to know. Each message contains only the critical

facts about new publications: a title, representative quote, a link to

the original, and our analysis in a sentence or two. To inquire or

subscribe, contact Damon at 206-283-7036 or

damon@centerltc.com.

Read testimonials by satisfied subscribers

here.

To subscribe online, please click

here.

LTC E-Alerts: Once a week, we compile our

daily LTC Clippings into a summary, email it to Center for Long-Term Care

Reform members, and archive it in The Zone, our password-protected

members-only website. Center members also receive our weekly LTC Bullet

op-ed. To join the Center and receive all these benefits and more,

contact Damon at 206-283-7036 or

damon@centerltc.com.

We no longer post our LTC E-Alerts on the

Center’s public access website, but here’s what today’s LTC E-Alert

contained: links, quotes and comments on the following articles, reports,

or data:

-

Data detail extent

of senior living and care provider reliance on immigrant workers

-

Sector challenges,

skilled nursing turnover present opportunity for first-time

entrepreneurs, ‘innovators’

-

BREAKING: CMS

unveils aggressive plan to fine, more easily expel noncompliant Medicare

providers

-

Lear's age of

suffering

-

Nearly Four

Million Medicare Beneficiaries Met the Eligibility Criteria in 2023 for

the Medicare GLP-1 Bridge

-

Medicare Advantage

by Default

-

Medicaid HCBS

growing, but worker wages falling, new study finds

#############################

"LTC E-Alerts" are

a

feature offered by the Center for Long-Term Care Reform, Inc. to members

at the $150 per year level or higher. We'll track and report to you news

and analysis regarding long-term care financing, service delivery, and

research. We hope The LTC E-Alerts will help you attain and maintain a

high level of knowledge and competency in this complex field. The

Center for Long-Term Care Reform, Inc. is a private institute dedicated to

ensuring quality LTC for all Americans (www.centerltc.com).

#############################

Updated Monday, June 29, 10:03 AM

(Pacific)

Seattle—

#############################

LTC

E-ALERT #26-022: LTC NEWS AND COMMENT

LTC

Comment: Do you spend hours searching the internet for useful articles,

key data, and relevant reports to keep you on the forefront of

professional knowledge? Do you lose business because you’re blindsided by

clients or competitors who learn critical information before you do?

Here’s an antidote:

LTC

Clippings: The Center for Long-Term Care Reform notifies subscribers to

our LTC Clippings service daily of information you need to know. Each

message contains only the critical facts about new publications: a title,

representative quote, a link to the original, and our analysis in a

sentence or two. To inquire or subscribe, contact Damon at 206-283-7036

or

damon@centerltc.com.

Read testimonials by satisfied subscribers

here.

To subscribe online, please click

here.

LTC

E-Alerts: Once a week, we compile our daily LTC Clippings into a summary,

email it to Center for Long-Term Care Reform members, and archive it in

The Zone, our password-protected members-only website. Center members

also receive our weekly LTC Bullet op-ed. To join the Center and receive

all these benefits and more, contact Damon at 206-283-7036 or

damon@centerltc.com.

We no

longer post our LTC E-Alerts on the Center’s public access website, but

here’s what today’s LTC E-Alert contained: links, quotes and comments on

the following articles, reports, or data:

-

John O’Connor and McKnight’s: A 36-year run

like no other

-

‘Confounding and heartbreaking’: Provider

groups decry Supreme Court decision that could see the departure of

immigrant workers

-

National Health Expenditure Projections,

2025–34: Strong Utilization Growth Initially, Legislative Impacts Later

-

Testimony of Bill Hammond on Medicaid’s

Consumer Directed Personal Assistance Program

-

Protecting Patients and Taxpayers:

Combating Healthcare Fraud and Leakage to Strengthen Program Integrity

-

What Surprises Aging Guru Ken Dychtwald

-

Americans Fear Navigating Long-Term Care

Alone More Than Affording It

-

I quit my job to care for my sick husband.

A little-known program provided training and pays me to do it

-

Political Insights from the 2026 Social

Security and Medicare Trustees’ Reports

#############################

"LTC E-Alerts" are

a feature

offered by the Center for Long-Term Care Reform, Inc. to members at the

$150 per year level or higher. We'll track and report to you news and

analysis regarding long-term care financing, service delivery, and

research. We hope The LTC E-Alerts will help you attain and maintain a

high level of knowledge and competency in this complex field. The

Center for Long-Term Care Reform, Inc. is a private institute dedicated to

ensuring quality LTC for all Americans (www.centerltc.com).

#############################

Updated Friday, June 26,

2026, 10:03 AM (Pacific)

Seattle—

#############################

LTC BULLET: LTC HOAX?

LTC Comment: The media and

researchers constantly misrepresent Medicaid LTC spend down. Is it a

genuine misunderstanding, a deliberate hoax, or something else? Answers

after the ***news.***

|

*** TODAY'S LTC BULLET is sponsored by Claude

Thau (BackNine Insurance). BackNine gives you a free

personalized website at no cost. Your clients (& family & friends)

can, with as little or as much of your involvement as you or they

want, buy life insurance and LTCi, and can speed issue by scheduling a

paramed and uploading medical records immediately. We quote

stand-alone LTCi, linked-benefit and life with a LTC rider

side-by-side. Claude is the lead author of Milliman’s annual Broker

World LTCi Survey & a past Chair of the Center for Long-Term Care

Financing. Contact him at 913-707-8863 or

claude@back9ins.com to learn about more

great BackNine features and services. *** |

*** CASE IN POINT: Here’s

the LTC Hoax in action. I penned the following letter to the editor of

Health Affairs about an article the journal published that gets

Medicaid LTC financial eligibility wrong. Of course, my letter wasn’t

published.

Here’s why.

Peer review is like a moat protecting the

LTC Narrative

that government is the solution to all LTC problems

Letter to the editor of

Health Affairs regarding “Medicaid Asset Limits And Enrollment

Among Older Adults And People With Disabilities” (https://doi.org/10.1377/hlthaff.2025.01437)

This article on Medicaid

asset limits displays a misunderstanding of Medicaid’s purpose and

operation in long-term care (LTC). Medicaid is not designed to promote

savings or minimize enrollment barriers; it is a safety net intended for

those who lack the means to pay for necessary care. To evaluate it through

the lens of enrollment friction obscures its core function.

The authors focus on

nominal asset limits, yet these limits are often circumvented in practice.

Applicants can convert countable assets into exempt forms—such as home

equity, personal property, or prepaid funeral expenses—allowing

individuals with substantial wealth to qualify. Similarly, income

eligibility rules permit high-income individuals to qualify once private

medical expenses are deducted. As a result, Medicaid LTC eligibility often

extends well beyond the truly needy.

The article’s empirical

findings—that some individuals who exceed asset thresholds are less likely

to enroll—are unsurprising and add little insight. More important is what

the analysis omits: how current rules enable middle- and upper-income

individuals to access publicly funded care while lower-income individuals

must spend down to near-total impoverishment before qualifying.

This dynamic has broader

consequences. More affluent individuals can access higher-quality

providers by paying privately before transitioning to Medicaid, while

providers must absorb lower reimbursement rates once that transition

occurs. This strains the care system and limits resources available for

the most vulnerable.

A more relevant line of

inquiry would examine why individuals with substantial assets can qualify

for Medicaid LTC at all, and how policy design might better align the

program with its intended role as a safety net for those most in need. ***

LTC BULLET: LTC HOAX?

I’ve wondered for years

how the actual results of Medicaid LTC spend down policy—easy access to

benefits while preserving wealth—can be so radically different from the

way they are presented in the media and scholarly publications, that is,

catastrophic spend down for care until total impoverishment. Do the

experts really not understand how Medicaid financial eligibility works? Or

do they know the truth but evade the reality because it doesn’t fit their

ideological proclivity toward government intervention? Perplexed, I

decided to enlist AI to help answer the question.

My Query to Gemini:

Medicaid financial

eligibility rules for long-term care (LTC) benefits allow people with high

incomes to qualify if their private medical or LTC expenses are

commensurately high because those private expenditures are deducted from

their income before the program's low income standard is applied.

Likewise, high asset people can qualify because most large assets seniors

own are exempt and countable assets are easily converted to exempt status

by simply using them to purchase non-countable resources. Unlike the

requirement for income spend down, that it be for documented private

health care expenses, however, there is no such requirement for asset

spend down. Asset spend down can be used to convert countable into

non-countable wealth in any amount. See “Medicaid’s

$100+ Billion Leak”

for details. Although this is true and indisputable, the conventional

wisdom repeated constantly in the media and often in scholarly sources is

that Medicaid LTC eligibility requires "impoverishment" and that people

all across America are spending down into destitution for LTC before they

qualify for Medicaid. Please give me a dozen or more examples of media or

academic sources that say Medicaid LTC eligibility requires

impoverishment. Then opine on why this mismatch between the reality and

the reporting persists decade after decade.

Gemini’s Answer:

You’ve identified a

significant gap between the technical reality of Medicaid planning and the

"impoverishment" narrative that dominates public discourse. Technically,

the "spend down" for assets does not require destitution in the way it is

often portrayed. Strategies like Medicaid Compliant Annuities, Caregiver

Agreements, and Equity-to-Exempt transfers allow for the preservation of

significant wealth. However, the media and academic framing consistently

emphasize a binary choice: pay out-of-pocket until broke, or qualify for

Medicaid only after reaching rock bottom.

Below are 12+ examples

of this narrative across mainstream media, advocacy groups, and academic

contexts.

Media & Journalism

These sources often

frame Medicaid LTC as a "safety net for the destitute," frequently

omitting the legal mechanisms used to protect assets.

- AP News

(2026): "Deliberately putting yourself or a relative into poverty so

Medicaid picks up the costs... Assistive living and nursing home care

often force families to exhaust their resources before qualifying." —

A Medicaid ‘spend down’ may get an older person LTC coverage.

- The New

York Times (2023): In various "Your Money" and "The New Old Age"

columns, the narrative often focuses on the "catastrophic" cost of care

that "drains life savings" to reach the $2,000 asset limit. Has referred

to the "Catch-22" of Medicaid where seniors must "spend down until they

are virtually penniless."

- CNBC

(2024): Business reporting frequently highlights that Americans are

"forced to spend down into poverty" to access long-term care benefits.

- KFF

(Kaiser Family Foundation): While technically accurate on rules,

their public briefs often headline the "limited financial resources" and

"low-income" nature of beneficiaries as a prerequisite.

- The

Washington Post: Often features op-eds or "Health & Science"

features describing the "vicious cycle of spending down every last cent"

to qualify for nursing home coverage. Reports on families "spending down

to the bone" to meet the $2,000 asset limit.

- Forbes:

While some articles discuss "Medicaid planning," many general finance

columns warn that LTC requires you to "impoverish yourself" to let the

government take over.

- The Wall

Street Journal: Often describes the "cruel choice" of "emptying the

bank account" to qualify for government help with long-term care.

- NPR:

Features stories on the "exhausting process" of "becoming poor enough"

to get Medicaid coverage for a spouse.

- PBS

NewsHour: Has framed segments on long-term care around the idea that

Americans must "become destitute to get help."

- CNBC:

Articles on retirement planning frequently warn that "long-term care can

impoverish you" before Medicaid kicks in.

Advocacy & Public

Interest Groups

These organizations

often use the "impoverishment" language to argue for better funding or

policy changes.

- AARP:

Frequently publishes guides stating that to qualify for Medicaid, you

must have "very little in the way of assets," reinforcing the idea that

the program is only for the poor.

- Center

for Medicare Advocacy: Highlights that current rules result in the

"impoverishment of older people and people with disabilities" due to the

high cost of out-of-pocket care. Notes that without spousal protections,

many would be "left with, literally, no income at all" and that

residents are "in jeopardy" of destitution.

- American

Health Care Association (AHCA): Often refers to the Medicaid

population in nursing homes as "low-income seniors" or "vulnerable

residents" who have no other options.

- Justice

in Aging: Focuses on the "economic insecurity" of seniors, framing

the eligibility process as a transition into poverty.

- NCOA

(National Council on Aging): Explains that "you must spend down

into poverty" to qualify for the Medically Needy program in many

states.

Academic & Policy

Research

Even in scholarly work,

the "Spend Down = Destitution" model is often the baseline assumption for

policy simulation.

- Health

Affairs: Numerous articles over the decades use the term "Medicaid

Spend-Down" as a synonym for the depletion of wealth by middle-class

seniors. Frequently discusses the "risk of impoverishment" for those

needing long-term services and supports (LTSS), framing the lack of

social insurance as a path to "financial destitution."

- Journal

of the American Medical Directors Association (JAMDA): Recent

studies emphasize that facilities are serving "the most impoverished

communities," linking Medicaid status directly to lack of wealth.

- The

Gerontologist: Academic papers frequently explore the "psychological

toll of spend-down," describing the process as one where seniors must

"bankrupt themselves" to get care. Research papers often categorize the

"medically needy" as those who have reached a state of "functional

poverty" through medical expenses.

- Urban

Institute: Policy briefs often describe Medicaid as the program for

those who have "exhausted their private resources" through the high cost

of long-term services.

- ASPE (HHS):

"Asset spend-down in nursing homes is the process by which

individuals... deplete their available assets... and then enroll in the

Medicaid program once they are impoverished." — A Synthesis

and Critique of Studies on Medicaid Asset Spenddown.

- Milbank

Quarterly: "Elderly persons with functional impairments must

impoverish themselves by incurring large out-of-pocket expenditures

on nursing-home care before becoming eligible for Medicaid benefits." —

Long-term Care, Medicaid, and Impoverishment of the Elderly.

- Journal

of the American Geriatrics Society (JAGS): Uses the term

"Medicaid-induced impoverishment" to describe the transition of

middle-class seniors into the program.

- Center

for Retirement Research (Boston College): Often frames studies

around the "likelihood of impoverishment" for retirees facing nursing

home stays.

-

Georgetown University (LTC Financing Project): Policy briefs

frequently state that Medicaid acts as a "safety net for those who have

exhausted their resources."

Key Nuance: The

"Myth" vs. The Narrative

There is a

counter-academic movement—most notably led by Stephen A. Moses of

the Center for Long-Term Care Reform—who has published extensively on

"The Myth of Medicaid Spend-Down."

The Reality:

While the media highlights the $2,000 asset limit, they rarely mention

that a primary residence (up to ~$700k–$1M+ depending on the

state), a vehicle, and irrevocable burial trusts are exempt.

Additionally, "Income Spend Down" is actually a "Spend Through," where the

applicant uses their income to pay their share of cost, while the

government covers the rest—hardly "destitution" if the care is being

provided.

The Reality vs. The

Narrative

As you noted, the

"indisputable" reality includes several legal avenues that prevent literal

destitution, yet they are rarely the focus of general reporting:

|

The "Impoverishment"

Narrative |

The Technical Reality |

|

"You must be penniless." |

You can keep a primary residence

(up to ~$713k–$1.07m equity), one car, and personal belongings. |

|

"You must spend all money on

care." |

You can spend "countable" cash

on "exempt" assets (e.g., home repairs, prepaying funerals, buying a

better car). |

|

"The spouse is left with

nothing." |

Spousal Impoverishment Rules (CSRA)

allow the community spouse to keep up to ~$154,140 in assets (2024/25

levels). |

|

"High income disqualifies you." |

"Income caps" can often be

bypassed via Miller Trusts (Qualified Income Trusts) in many states. |

LTC Comment:

Follow up: based on your

findings, do you think this commonplace misrepresentation of the reality

is intentional to support an ideological bias or based only on ignorance?

AI:

The gap between the "impoverishment" narrative and the actual

mechanics of Medicaid eligibility isn't easily reduced to just a

malicious lie or just simple ignorance. Instead, it is a classic

example of structural bias—where institutional complexities, media

incentives, and political ideologies converge to create a distorted public

perception.

If you analyze the behavior of the groups

pushing this narrative, you can see a mix of well-meaning

oversimplification, strategic political positioning, and

commercial interest.

Here is how the motivations break down

across the spectrum:

1. The Media: The "Path

of Least Resistance" & Human Drama

For journalists, the misrepresentation is

driven less by a deep ideological conspiracy and more by occupational

constraints:

- Complexity: Medicaid is a

labyrinth of federal guidelines and 50 distinct sets of state rules.

Explaining "Medically Needy" income spend-down or the mechanics of a

Qualified Income Trust (Miller Trust) requires too many column inches

and bores the general reader.

- The "Unplanned" Reality: For the

vast majority of middle-class families who do not hire an elder

law attorney in advance, the experience feels like

impoverishment. They enter a crisis (e.g., a sudden stroke), go to a

nursing home, and are told they must pay $10,000/month out-of-pocket

until their liquid bank accounts hit $2,000. That is the story that

reaches reporters. The reporter writes about the crisis, missing the

fact that a proactive lawyer could have sheltered those assets.

- Narrative Arc: "Local senior

forced into poverty by broken healthcare system" is a compelling,

high-engagement headline. "Local senior successfully shifts wealth into

exempt asset categories using legal loopholes" is a technical financial

column.

2. Left-Leaning Academics

and Policy Advocates: Supporting Universal Care

For progressive think tanks and advocates,

framing Medicaid as requiring "impoverishment" serves a specific

ideological goal: the expansion of the social safety net.

- The Goal: They want a universal,

Medicare-for-all-style long-term care benefit.

- The Strategy: To build political

will for universal care, you must convince the middle class that they

too are at risk. If the middle class believes they can easily

navigate Medicaid rules to protect their inheritances, they won't vote

for expensive new government programs. By highlighting the $2,000 asset

limit and framing it as "destitution," they create pressure for systemic

reform.

3. Right-Leaning/Fiscal

Conservative Groups: Highlighting Welfare Abuse

Conversely, some conservative groups

actually agree with your premise—that Medicaid is easily

manipulated—but they use it to argue for stricter asset recovery and

tighter rules:

- They argue that middle-class or wealthy

seniors are "crowding out" the truly poor by hiding wealth in exempt

assets (like high-value homes or annuities).

- However, when these groups write

public-facing warnings, they often emphasize the "harshness" of the

rules to discourage people from relying on Medicaid, unintentionally

reinforcing the narrative that the program is punitive.

4. The Elder Law and

Long-Term Care Insurance Industries

There is a massive commercial incentive to

keep the "impoverishment" narrative alive:

- Long-Term Care Insurance (LTCI)

Companies: To sell a policy, they must terrify you. Their marketing

materials constantly declare: "A nursing home will wipe out your life

savings and leave you destitute!" They rarely mention that a good

attorney can shelter your assets without their insurance.

- Elder Law Attorneys: Ironically,

even though these lawyers specialize in proving Medicaid doesn't require

destitution, their marketing often leads with the threat of

impoverishment to get clients through the door: "Don't let the

nursing home take your house!"

Summary: Ignorance

Filtered Through Incentives

The Verdict: It is rarely pure,

conscious ignorance, but rather strategic framing.

Every player in the ecosystem has a reason

to emphasize the "scary" $2,000 cash limit rather than the "lenient"

exempt asset rules:

- Advocates want to show the

system is cruel so it will be changed.

- Journalists want a dramatic

story about human suffering.

- Businesses want to sell you a

product (insurance or legal services) to protect you from that cruelty.

The legal reality you pointed out—that a

senior can buy a $500,000 exempt home, buy a brand new car, pay off a

mortgage, and prepay funerals to qualify for Medicaid—is an open secret

among lawyers, but a deeply inconvenient truth for almost every major

narrative or commercial interest in the space.

Closing LTC Comment: Well, there

you have it. Misrepresenting Medicaid financial eligibility policy to

suggest it requires spend down into impoverishment is not a hoax

(deliberate deceit) according to AI, but only different groups pursuing

their self-interests. Smooth, I say. That lets everyone off the hook of

thinking about what would be better public policy. Maybe you can excuse

senior advocates and business enterprises for pursuing their narrow

interests. But should we exonerate Medicaid planners who manipulate the

rules to help affluent clients for big fees at the expense of the

genuinely needy? Should scholars who ought to pursue objective truth get a

pass? No, I think the term “LTC Hoax” applies accurately to them. They

allow a self-serving lie to take precedence over truthful analysis in

pursuit of better public policy.

To make sense of what ails LTC, read the

Paragon Health Institute’s “Long-Term

Care: The Problem” and “Long-Term

Care: The Solution” and watch this “virtual

LTC event” featuring age wave visionary Ken Dychtwald and leading LTC

researchers. To find ample private funds for LTC, check out “Medicaid’s

$100+ Billion Leak.” For what not to do, see “Medi-Cal-amity:

California’s Reckless Expansion of Medicaid Long-Term Care to the Affluent.”

See also “Better

Long-Term Care for Billions Less.” Find much more on long-term care

here.

#############################

Updated

Monday, June 22, 10:03 AM (Pacific)

Seattle—

#############################

LTC E-ALERT #26-021: LTC NEWS AND COMMENT

LTC Comment: Do you spend hours searching

the internet for useful articles, key data, and relevant reports to keep

you on the forefront of professional knowledge? Do you lose business

because you’re blindsided by clients or competitors who learn critical

information before you do? Here’s an antidote:

LTC Clippings: The Center for Long-Term

Care Reform notifies subscribers to our LTC Clippings service daily of

information you need to know. Each message contains only the critical

facts about new publications: a title, representative quote, a link to

the original, and our analysis in a sentence or two. To inquire or

subscribe, contact Damon at 206-283-7036 or

damon@centerltc.com.

Read testimonials by satisfied subscribers

here.

To subscribe online, please click

here.

LTC E-Alerts: Once a week, we compile our

daily LTC Clippings into a summary, email it to Center for Long-Term Care

Reform members, and archive it in The Zone, our password-protected

members-only website. Center members also receive our weekly LTC Bullet

op-ed. To join the Center and receive all these benefits and more,

contact Damon at 206-283-7036 or

damon@centerltc.com.

We no longer post our LTC E-Alerts on the

Center’s public access website, but here’s what today’s LTC E-Alert

contained: links, quotes and comments on the following articles, reports,

or data:

-

What is Socialism?

-

‘Will I spend my 50s or 60s as a caregiver?’: A

woman in an age-gap relationship started doing 'grief math' — and it

exposed a financial blind spot

-

Senior living communities charging more for the

room, less for the care

-

5 Contentious Reasons the Middle Class Hasn't

Bought Long-Term Care Insurance

-

Social Security Is In Far Worse Shape Than We're

Being Told: The System's $71.9 Trillion Unfunded Liability Is Over Twice

What its ‘Trustees’ Mention

-

Spending on Medicaid State Directed Payments Before

New Limits Take Effect

-

Federal Medicaid Spending Through State Directed

Payments Nears $100 Billion Annually Across 41 States, With New Limits

Set to Reduce Funding to States

-

Senior living industry backs new CMS Medicaid

waiver oversight rules

#############################

"LTC E-Alerts" are

a

feature offered by the Center for Long-Term Care Reform, Inc. to members

at the $150 per year level or higher. We'll track and report to you news

and analysis regarding long-term care financing, service delivery, and

research. We hope The LTC E-Alerts will help you attain and maintain a

high level of knowledge and competency in this complex field. The

Center for Long-Term Care Reform, Inc. is a private institute dedicated to

ensuring quality LTC for all Americans (www.centerltc.com).

#############################

Updated Monday, June 15, 10:03 AM

(Pacific)

Seattle—

#############################

LTC

E-ALERT #26-020: LTC NEWS AND COMMENT

LTC

Comment: Do you spend hours searching the internet for useful articles,

key data, and relevant reports to keep you on the forefront of

professional knowledge? Do you lose business because you’re blindsided by

clients or competitors who learn critical information before you do?

Here’s an antidote:

LTC

Clippings: The Center for Long-Term Care Reform notifies subscribers to

our LTC Clippings service daily of information you need to know. Each

message contains only the critical facts about new publications: a title,

representative quote, a link to the original, and our analysis in a

sentence or two. To inquire or subscribe, contact Damon at 206-283-7036

or

damon@centerltc.com.

Read testimonials by satisfied subscribers

here.

To subscribe online, please click

here.

LTC

E-Alerts: Once a week, we compile our daily LTC Clippings into a summary,

email it to Center for Long-Term Care Reform members, and archive it in

The Zone, our password-protected members-only website. Center members

also receive our weekly LTC Bullet op-ed. To join the Center and receive

all these benefits and more, contact Damon at 206-283-7036 or

damon@centerltc.com.

We no

longer post our LTC E-Alerts on the Center’s public access website, but

here’s what today’s LTC E-Alert contained: links, quotes and comments on

the following articles, reports, or data:

-

A New Option for Long-Term Care Costs

-

Advisors Aren't Ready For The 30-Year

Retirement, Ken Dychtwald Argues

-

Medicare Advantage Organizations overturned

most SNF denials, OIG finds

-

The Nation's Fiscal Health: Urgent and

Sustained Action Needed to Improve the Fiscal Outlook

-

What’s in the 2026 Medicare Trustees

Report?

-

Social Security funds could run short by

2032, program's Trustees warn

-

A Closer Look at the IRS LTC Guidance

-

What to Know About Recent Federal Actions

Involving State Medicaid Program Integrity

-

Ohio suspends 49 home health providers from

Medicaid program over fraud concerns

-

Long-term care reform plans spark

widespread backlash in Germany

#############################

"LTC E-Alerts" are

a feature

offered by the Center for Long-Term Care Reform, Inc. to members at the

$150 per year level or higher. We'll track and report to you news and

analysis regarding long-term care financing, service delivery, and

research. We hope The LTC E-Alerts will help you attain and maintain a

high level of knowledge and competency in this complex field. The

Center for Long-Term Care Reform, Inc. is a private institute dedicated to

ensuring quality LTC for all Americans (www.centerltc.com).

#############################

Updated Friday, June 12, 2026, 10:03 AM (Pacific)

Seattle—

#############################

LTC BULLET: WHAT IS

MEDICAID FOR?

LTC Comment: These

scholars publishing in a peer-reviewed journal do not understand

Medicaid’s purpose, nor how it hurts the poor and helps the well-to-do. We

explain after the ***news.***

*** Share Your Working Caregiver Story

CareScout and Genworth, in partnership with Share

More Stories, are inviting working caregivers to participate in a

storytelling-based research project focused on the real experience of

balancing work and caregiving.

By sharing an audio or written story through the SEEQ

platform, caregivers can help deepen understanding of the emotional and

practical realities they face, and contribute to more effective support(s)

in the future.

Eligible participants receive a $25 gift card.

Learn more and participate:

https://sharemorestories.com/working-caregiver-experience-carescout-seeq/

***

LTC BULLET: WHAT IS

MEDICAID FOR?

LTC Comment: The

following article in the current issue of Health Affairs is a

confused mishmash of mistaken notions that never should have passed peer

review. The complete piece does not deserve your attention, but the

abstract is worth our brief scrutiny. It displays the confusion, common

among Medicaid LTC researchers, regarding the Medicaid program, its

legitimate purpose and how it diverges in practice from official

objectives. Here’s the article, its abstract, and our line-by-line review.

“Medicaid

Asset Limits and Enrollment Among Older Adults and People With

Disabilities,” by Andrew Anderson, Chau

Huynh, and Catherine K. Ettman, Health Affairs, 45, NO. 6 (2026):

708–715.

ABSTRACT Medicaid asset

limits determine how many countable resources older adults and people with

disabilities may retain while qualifying for coverage. Although intended

to target benefits to those with the greatest financial need, these rules

may discourage saving and create administrative barriers to enrollment.

Amid recent federal and state reforms to update asset limits and a new

federal home equity cap of $1 million taking effect in 2028, we examined

how many income-eligible older and disabled adults are affected by

Medicaid asset limits and whether exceeding these limits is associated

with lower enrollment. Using nationally representative data for 2023, we

estimated that among 6.2 million income-eligible adults not enrolled in

Medicaid, 1.5 million (24.7 percent) exceeded their state’s financial

asset limit and 387,525 (8.6 percent) exceeded the home equity limit.

Regression discontinuity models indicated that exceeding financial asset

thresholds was associated with lower enrollment among unmarried adults.

Asset limits thus exclude a modest share of otherwise-income eligible

people overall but may disproportionately burden subgroups with limited

financial resources.

LTC Comment:

Let’s dissect this abstract sentence by sentence to see if we can make

sense of it, or at least explain what it gets wrong.

Abstract:

“Medicaid asset limits determine how many countable resources older adults

and people with disabilities may retain while qualifying for coverage.”

LTC Comment:

This is true and the limit on countable resources is usually very low,

often $2,000. But the official limit is irrelevant because there is no cap

on how much countable wealth applicants can convert to non-countable

status simply by purchasing exempt assets. Pay off a mortgage or add a

room to increase home equity, buy a nicer car, prepay funeral expenses,

purchase expensive new personal and household belongings, acquire a

business or rental property, and so on. There is practically no limit to

how much wealth the affluent can shelter and retain in this way. See “Medicaid’s

$100+ Billion Leak for details.”

Abstract:

“Although intended to target benefits to those with the greatest financial

need, these rules may discourage saving and create administrative barriers

to enrollment.”

LTC Comment:

What a peculiar notion. The purpose of Medicaid is not to encourage

savings or avoid administrative barriers to enrollment. It is to provide a

financially viable safety net of LTC services for people who have failed

to save and have become a financial and administrative burden on the

state. Medicaid should target benefits to those most in need and exclude

others of lesser or no need. These authors have Medicaid’s role upside

down and backwards.

Abstract:

“Amid recent federal and state reforms to update asset limits and a new

federal home equity cap of $1 million taking effect in 2028, we examined

how many income-eligible older and disabled adults are affected by

Medicaid asset limits and whether exceeding these limits is associated

with lower enrollment.”

LTC Comment:

What kind of question is that? If exceeding asset limits is not associated

with lower enrollment, something is obviously wrong. Otherwise, why set

limits on assets in the first place? Regarding the million dollar home

equity limit, it prevents very few people from qualifying for Medicaid LTC

benefits because the median home equity of elderly Americans,

$250,000, is only one-fourth of that

amount. A better research question would be: how many people with home

equity approaching a million dollars receive welfare-financed Medicaid

benefits and why is that allowed?

Abstract:

“Using nationally representative data for 2023, we estimated that among